The fiercest competition between Presidents Donald Trump and Xi Jinping in 2025 seemed to involve who could stop US imports from China the fastest. Trump started early and went big. He launched his second trade war soon after taking office in January and raised tariffs on China by 145 percentage points by April. By June, US imports from China were roughly half their levels of a year earlier, falling to depths not seen since the financial crisis of 2009.

Xi responded by restricting Chinese exports. Twice in 2025, he nearly brought the US automobile industry to a screeching halt by cutting off companies’ access to essential Chinese inputs. With nearly 6.5 percent of US manufacturing workers employed in just-in-time automotive supply chains, the economic disruption could have been traumatic.

The two countries eventually called a truce and some trade resumed. US auto production that had been paused was able to restart. But the direction of travel is clear: Trade between the two countries is unwinding faster than ever. Before Trump’s first trade war started in 2018, 22 percent of US goods imports were from China. By the end of 2025, China’s share had fallen to 9 percent, down 4 percentage points from the beginning of the year alone.

Meanwhile, America's real imports from the rest of the world rose 9 percent in 2025. That may seem surprising, given that Trump had applied tariffs on all these other countries too. But the duties slapped on Chinese exports were mostly higher than those on others, and many businesses adapted by moving supply chains out of China to alternative locations, including Vietnam, Taiwan, and Mexico. And US imports of products needed to build out data centers for artificial intelligence also boomed.

Yet for a final group of more stubborn products, supply chains have yet to leave China. Xi weaponized two of those—rare earth permanent magnets and certain semiconductors—in 2025. The consequences were frightening for carmakers and workers worldwide who remain heavily dependent on China for such vital inputs.

Given all the trade policy drama that unfolded during the first year of Trump’s second trade war, here are five things to know from the 2025 US import data.

1. In 2025, the US imported much less from China and more from others

US imports from the world held up in 2025, rising 4 percent in real terms compared to 2024 (figure 1). Despite the new president’s global tariffs, imports remained even above the trend growth rate established before his first trade war began in July 2018. Americans did begin to load up on imports after Trump won the November 2024 election in anticipation of his coming tariff barrage. But much more was at play.

US imports from China alone are quite a different (and longer) story. That tale began with imports falling shortly after Trump commenced his first trade war in July 2018. US imports from China temporarily ticked up during the pandemic, driven by a surge in demand, as locked down Americans desperately raced to buy Chinese-made goods ranging from face masks to toys to consumer electronics. As COVID-19 receded, so did US imports from China, leveling off in late 2023. And though trade temporarily increased again after the 2024 election, as importers built up inventories in anticipation of a second Trump tariff barrage, the boost was short lived.

Trump’s new tariffs on China in 2025 came in fast, high, and comprehensive. Only seven weeks into his new administration, he had raised tariffs by 20 percentage points on all imports from China. (This increased the average US tariff on China by more than all the tariffs imposed during his entire first term.) These new tariffs lasted most of the year and were distinct from the tariff escalation and retreat of April and May, when Trump temporarily raised tariffs on China by another 125 percentage points. All told, the average US tariff on imports from China remained at nearly 50 percent through the end of 2025, up from 21 percent on January 20, 2025—Trump’s second inauguration day.

Real US imports from China dropped by 28 percent in 2025 alone. They ended up 40 percent lower than they were on the eve of Trump’s first trade war in 2018 (see again figure 1). The first half of that decline was a slow burn, taking nearly seven years. The second half was more like lightning, taking only seven months following Trump’s second tariff escalation.

Trump also put tariffs on the rest of the world’s economies in 2025. For them, he increased the average US tariff from 3 percent to over 18 percent. (Trump’s first term tariffs focused almost exclusively on China.) Even so, real imports from countries other than China rose more than 9 percent in 2025 (see again figure 1). Since 2017, China’s share of US imports has declined by over 12 percentage points, largely at the expense of Taiwan (4.1 points), Vietnam (3.7 points), and Mexico (2.3 points).

2. Trump’s first trade war continued to affect US imports from China in 2025

Heading into Trump’s second inauguration, the effects of his first term tariffs lingered in expected ways (figure 2). Chinese products hit with high (25 percent) tariffs in 2018–19 had suffered the most: Having dropped immediately upon impact, they were about 40 percent lower in January 2025 than in June 2018. US imports from China of goods that Trump had spared from his first term tariffs had increased and sat 16 percent higher.

That all changed with Trump’s January 2025 return. With his new tariffs hitting all products from China this time, the sharpest import decline came in those goods that had originally been spared from the duties of his first term. By the end of 2025, these imports were now 25 percent below June 2018 levels. (Still economically important, these products made up 45 percent of total US imports from China in 2024.) Imports from China of the other products also fell in 2025, just by less, partly because their supply chains had started moving earlier.

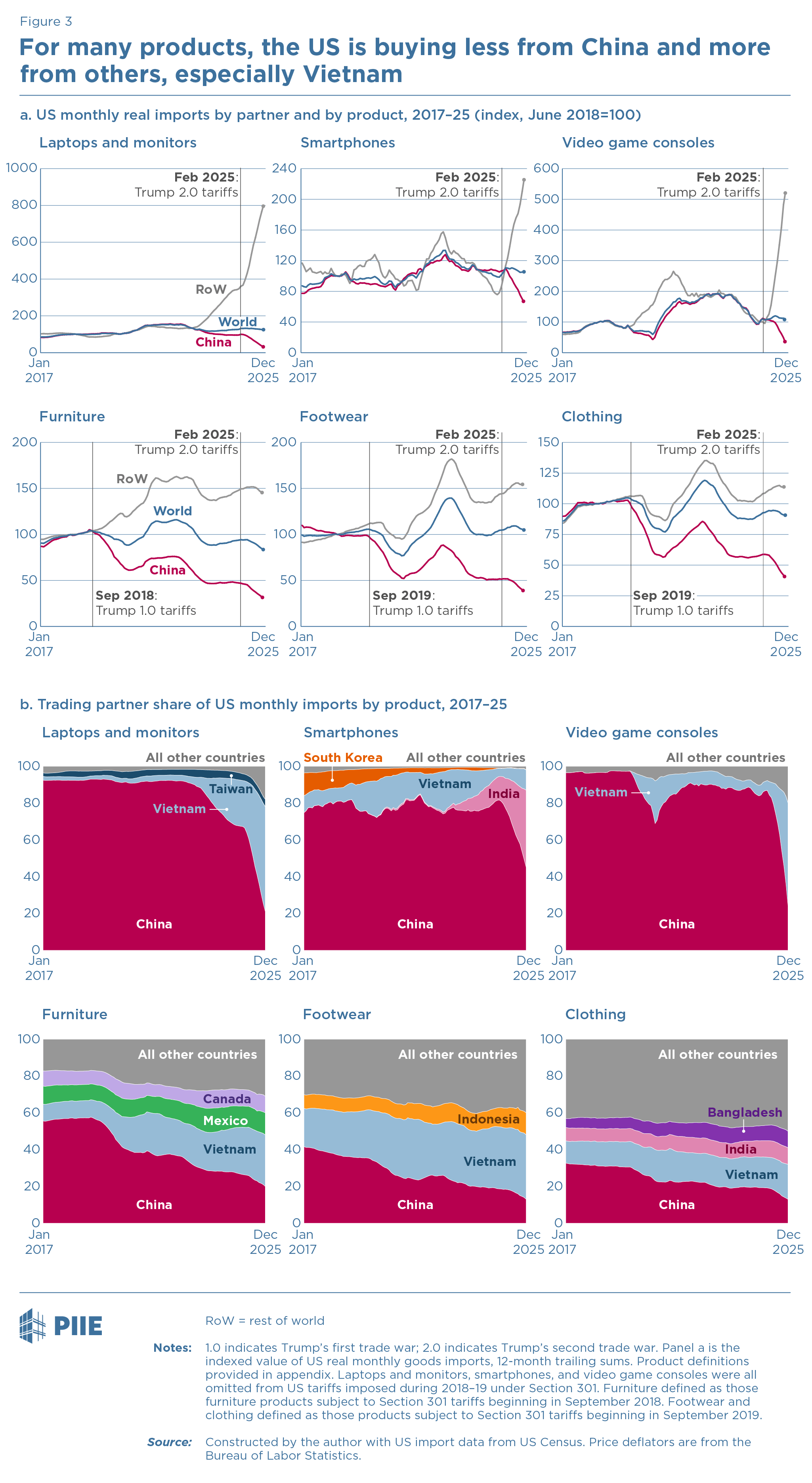

3. Supply chains have moved out of China at different speeds

Start with some of the consumer electronics omitted from Trump’s tariffs in 2018–19. At the time of his second inauguration, US imports from China of laptops and monitors, smartphones, as well as video game consoles all remained at or above their levels before his first trade war (figure 3a). After Trump applied his 20 percent tariffs in 2025, imports from China of game consoles, as well as laptops and monitors, fell by 70 percent. Smartphones fell by 40 percent.

Surprisingly, total US imports of these consumer electronics weathered the 2025 tariff storm. Despite the massive and sudden decline in sourcing from China, real imports of each from the world were relatively flat in 2025, even remaining above the levels preceding the first Trump trade war.

The process may seem simple. When China gets hit with a higher tariff, firms leave and invest in factories elsewhere to export to the US market. Before Trump’s first trade war, China provided over 90 percent of US imports of video game consoles, as well as laptops and monitors (figure 3b). Over 80 percent of imported smartphones came from China. By the end of 2025, China’s share had dropped considerably. (For game consoles, as well as laptops and monitors, the fall was over 70 percentage points.)

Vietnam turned out to be an important alternative source for each product. Though Trump’s first term tariffs did not hit these consumer electronics, major multinationals eventually invested in new supply chains anyway. (When the Biden administration did not reverse Trump’s other tariffs on China between 2021 and 2024, the message had become clear.) Dell and Apple turned to Vietnam for laptop assembly. Sony, Nintendo, and Microsoft set up contractors in the country to manufacture the PlayStation, Switch, and Xbox. Only smartphones proved slightly different. While Korean brands like Samsung and LG had long assembled some of their phones in Vietnam, Apple developed iPhone assembly facilities in India.

The shift for these products was speedy in 2025. When Trump hit Chinese-manufactured electronics with tariffs for the first time in February and March, alternative foreign assembly plants were ready. US imports from non-Chinese sources in 2025 ended up more than twice as high for laptops and monitors, nearly three times as high for smartphones, and more than five times as high for gaming consoles (figure 3a). (It helped that Trump excluded products like smartphones and laptops from most of the new tariffs he applied on non-Chinese suppliers in 2025.)

Many products hit by Trump’s first term tariffs had begun moving earlier. By the eve of Trump’s second inauguration, US imports from China of furniture and footwear, for example, had already dropped by roughly half (figure 3a). When hit with additional tariffs in 2025, they fell but by much less.

Vietnam was also often an important new US supplier for these products. The country nearly tripled its share of US furniture imports between June 2018 and 2025 (figure 3b). In addition to Vietnam, the United States now imports relatively more of its footwear from Indonesia, Cambodia, and Thailand, as well as its clothing from Bangladesh and India.

The emergence of new supply chain investments to service the US market also explains why many of these South Asian countries were so eager to make early deals with the Trump administration in 2025 that would lock in their relative tariff advantage over China. Even though South Asia faced higher rates than in 2024, at least their firms continued to face lower US tariffs for these products than companies in their key competitor.

Nevertheless, new foreign sources could not always fully make up for the sudden additional loss of imports from China in 2025. Total US imports of these furniture and clothing products ended up significantly lower than their levels prior to the first trade war. (Footwear remained only 5 percent higher.) Unlike in 2018–19, suddenly these other countries were facing higher US tariffs for some of these products too.

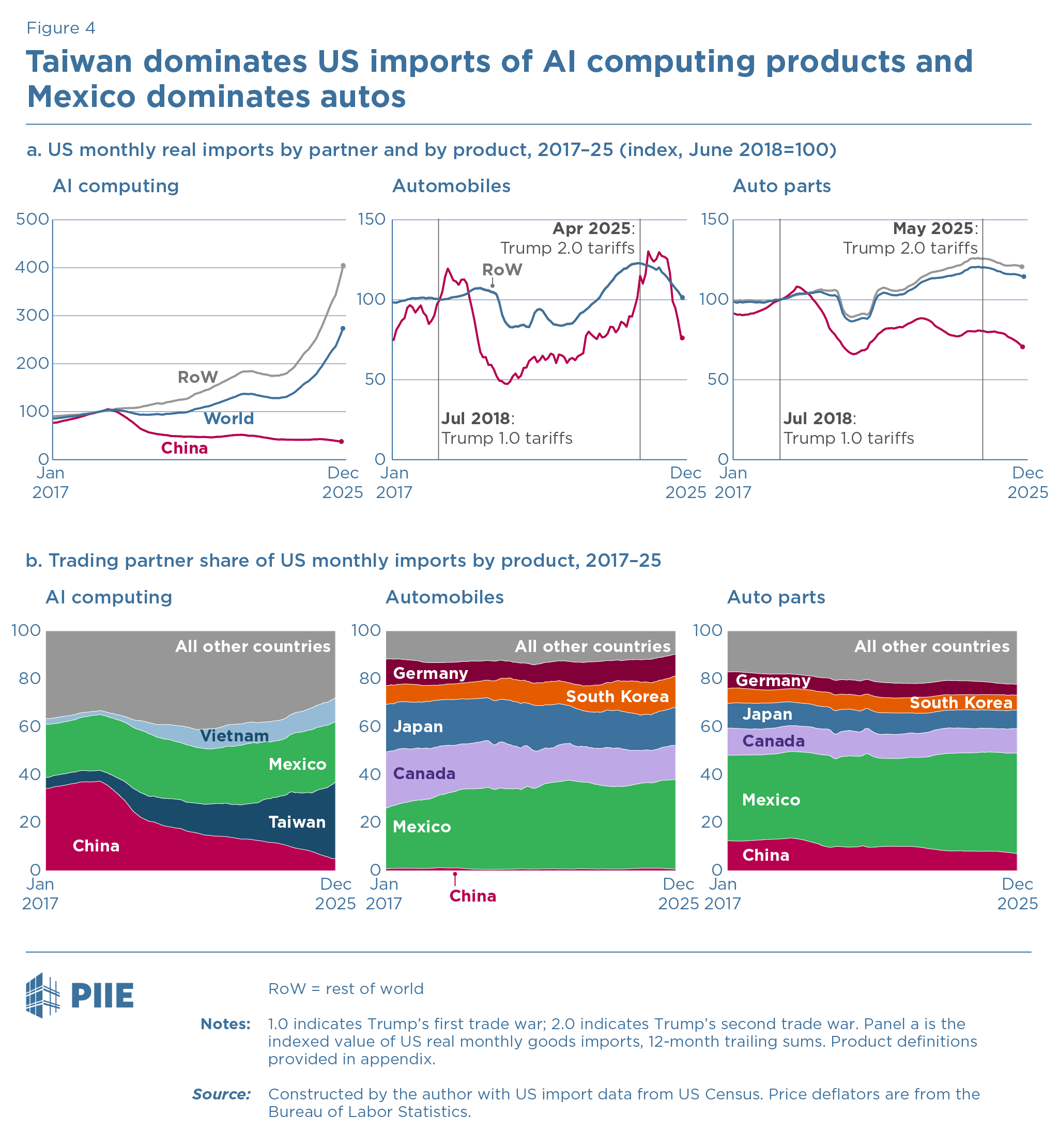

4. Taiwan dominates US imports of computing products for AI, while Mexico dominates cars

Like Vietnam, Taiwan and Mexico have also emerged as increasingly important suppliers of US imports since 2017. Their stories why are slightly different.

Artificial intelligence (AI) helps explain the rising importance of Taiwan and, to a lesser extent, Mexico. The Taiwan Semiconductor Manufacturing Company (TSMC) has dominated global production of advanced node chips, designed by American firms like Nvidia and Advanced Micro Devices (AMD), needed to power computing for AI. Until recently, TSMC was only manufacturing these semiconductors at its facilities in Taiwan. Their chips would be combined with others, including high-bandwidth memory (produced by SK Hynix, Micron, or Samsung), put onto printed circuit boards, then added to racks for servers by companies like Taiwan’s Foxconn, to be shipped for final assembly and installation in the data centers now popping up all over the United States.

US imports of these AI computing products skyrocketed in 2025 especially (figure 4a). By one estimate, the $177 billion annual increase was larger than the overall jump in US imports of all goods from all countries in 2025 ($144 billion, in real terms). Taiwan has been the primary source of that increase (figure 4b). Put differently, the estimated increase in imports of AI-computing products from Taiwan alone was responsible for over half of the increase in total US imports of all goods from all countries in 2025.

Mexico’s substantial increase in its share of US imports has also been driven by the AI data center boom in the United States. US imports of AI computing products from Mexico jumped in 2025 as well, making up over one quarter of the increase in total annual US imports. (In 2024, Foxconn had announced it was building the world’s largest AI server assembly plant for Nvidia in Mexico.) Mexico’s focus on assembly means that it is likely capturing much less of the value-added than Taiwan, which is also manufacturing the underlying chips. Nevertheless, US demand for AI helps explain the relative export successes of Taiwan and Mexico in 2025.

US automotive imports were a less successful story in 2025. The Trump administration applied a 25 percent tariff on imports from all countries of autos in April and auto parts in May. This had a negative impact on imports of both segments of the industry, especially for automobiles (figure 4a). There were no winners in 2025, as imports from all major sources declined.

Yet Mexico has become a more important source of US auto imports over time (figure 4b). Since 2017, Mexico’s share of the US import market has increased by 12 percentage points for finished vehicles and 6 points for parts. Even though Chinese cars have come to dominate world markets, they continue to be kept out of the United States by steadily rising US tariffs since 2018. Mexico’s increased share of US imports of vehicles has thus come at the expense of Canada (down 9 points) and Japan (down 4 points). Mexico’s relative gains in this economically sizeable sector since 2017 also helps explain its overall increase in US import market share over the period.

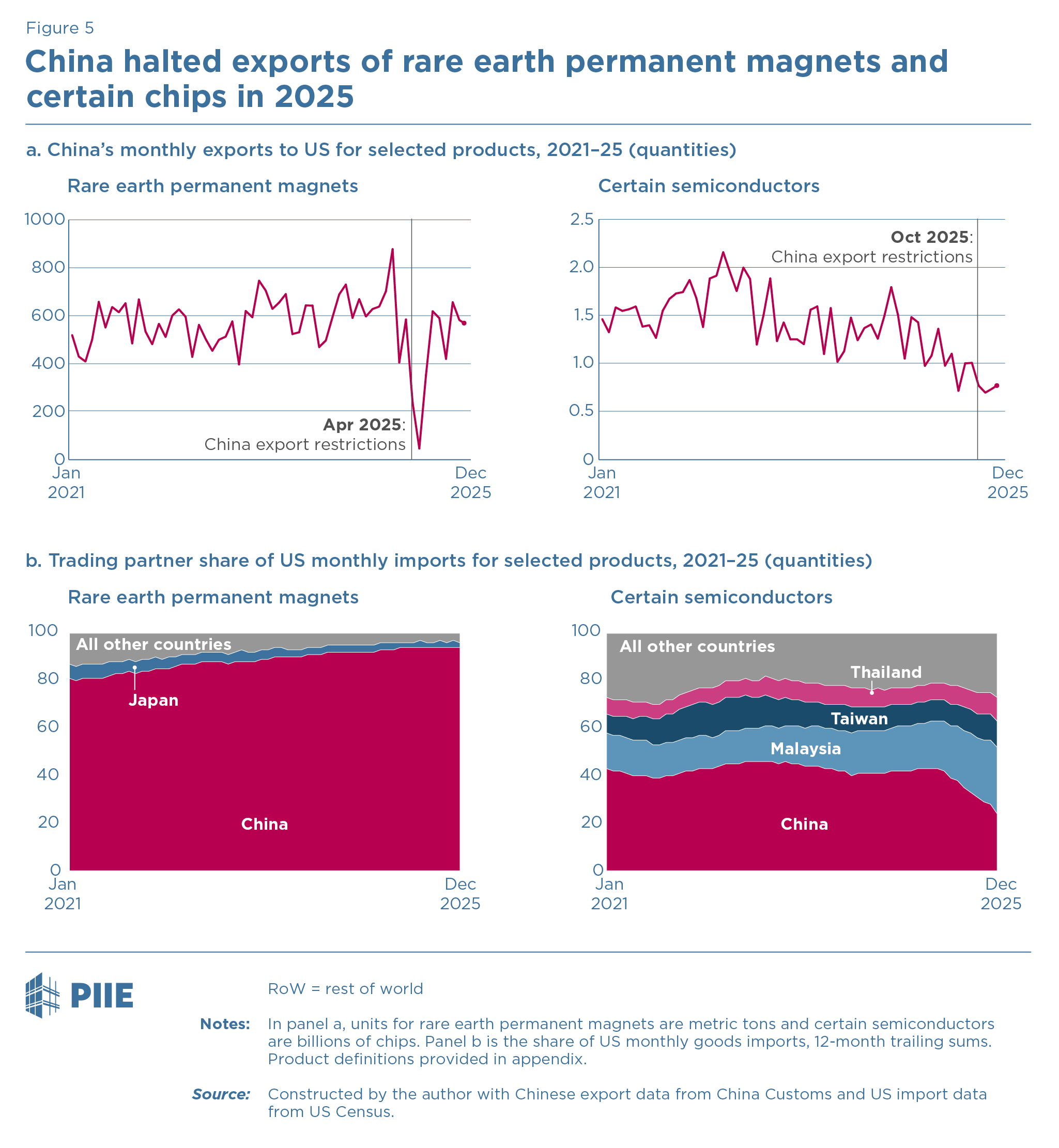

5. Some supply chains have yet to move out of China, with consequences

In response to Trump’s early 2025 tariff escalation, on April 4, Xi suddenly restricted exports of rare earth permanent magnets to the world. Monthly exports to the United States fell to nearly zero in May (figure 5a).

Cut off from imports of rare earth permanent magnets, the US auto industry went into panic mode. “We have had to shut down factories. It’s hand-to-mouth right now,” Ford CEO Jim Farley said in a June interview with Bloomberg. (With over 800,000 workers, the auto supply chain makes up nearly 6.5 percent of all manufacturing jobs in the United States.) Car companies needed the magnets to make seats, motors, windshield wipers, and audio systems work. And since the Chinese export restrictions were global, the United States could not look for parts elsewhere, as automakers in Europe, Japan, and even India had to shut down production too. Eventually the United States and China negotiated a deal, and by July, the magnet exports to the United States were back to more normal levels.

When the Trump administration raised tensions again, in October, the Chinese government suddenly stopped exports of a second essential input to the auto industry. (The escalation arose when Washington expanded its export restrictions to cover subsidiaries of Chinese companies already subject to US controls.) Beijing halted exports of semiconductors made by Nexperia. The global automotive industry relied on those chips to power braking systems, airbags, electric windows, and more.

For the second time in less than six months, car makers faced a sudden supply chain crisis. Honda had to temporarily shut down some of its North American production lines and adjust others. Stellantis set up a “war room” to deal with the prospect of shortages. Only when Trump and Xi met in late October in South Korea did China agree to allow shipments from Nexperia to resume.

The effects of China shutting down those semiconductor exports are much more difficult to observe in the data (figure 5a). Beijing apparently did not restrict exports from all Chinese companies making similar chips, only Nexperia. Yet, even if it had, the publicly available information about semiconductor trade is often not sufficiently informative to identify vulnerabilities. For example, trade data does not split out semiconductors either by end use (e.g., chips needed for car parts versus AI) or by vintage (e.g., mature node versus advanced node).

These data were also not useful because they did not reveal that the United States depended on China for these types of chips (figure 5b). Although the automakers revealed through their actions that they were very reliant on Nexperia, these data alone suggest China was the source of only 40 percent of US imports. Why weren’t Malaysia and Thailand, for example, an alternative source of such chips?

Automakers form long-term relationships with their suppliers. Chips for cars require testing to ensure safety and durability, since auto parts must work in extreme weather conditions and for the life of the car. It takes time to qualify a new chipmaker. Nevertheless, the Nexperia saga highlights why policymakers also worry that companies remain uninformed about their own vulnerabilities. (In 2024, a US government survey of companies revealed 44 percent did not know if their chips were coming from China.)

If the Nexperia vulnerability was hard to observe in the data, the rare earth permanent magnets case was not. According to the International Energy Agency, China accounted for over 90 percent of global production of neodymium (rare earth) magnets in 2024, as well as over 90 percent of production (both mining and processing) of the underlying rare earth elements. These vulnerabilities are also clearly visible in the US import data (figure 5b). (In April 2025, China also restricted its exports to the world of the rare earths that potential alternative suppliers in Japan would also need to make magnets.)

Since permanent magnets and rare earths had long flashed warning lights, the main puzzle was why the Trump administration dismissed indicators of this vulnerability and went ahead with its escalatory tariff actions toward China in early 2025 anyway.

After the Supreme Court rejection, what’s next for Trump’s Tariffs?

The US Supreme Court’s February 2026 ruling against many of Trump’s 2025 tariffs forced him to recalibrate his entire trade strategy. In March 2026, the Trump administration announced new investigations into allegedly unfair trading practices by China, Vietnam, Taiwan, Mexico, Japan, the European Union, and dozens of other economies under Section 301 of the Trade Act of 1974. While new tariffs are a likely outcome of these investigations, the 2025 US import data reveal how the details of US policy matter. Keeping higher tariffs on China than on other countries, for example, would incentivize companies that have moved supply chains out of China to retain them in their new locations.

Equally important to global economic security and US imports may be Trump’s other policy decisions in 2026. China has developed market dominance over much more than Nexperia’s chips, permanent magnets, and rare earths. Companies around the world remain subject to hidden supply chain vulnerabilities that Beijing has now shown it can and will weaponize. Yet there is often no viable American source as an option. The Trump administration will need to work with other countries to create alternative sources of supply quickly and efficiently.

The administration may have finally recognized this danger and begun to act on it. In early 2026, the United States convened dozens of countries and hosted two separate ministerial meetings on critical minerals. While the ultimate policy details of this initiative are important, real progress on US economic security requires something else. In setting his post–Supreme Court decision trade agenda, Trump will need to prioritize lowering tariffs on these same partners and allies. Asking them to do some of the hard work necessary to address concerns over Chinese market dominance across a range of industries requires important policy change by the United States as well.

With the easy bits of US-China supply chain decoupling now over, the hard-to-move parts remain. Trump’s 2026 policy decisions have the potential to affect much of the world’s economic security. If he gets them wrong, for other industries with hidden vulnerabilities, the worst may be yet to come.

Appendix

See the disclosed data file for the product codes and price deflators used in the analysis.

Data Disclosure

Related Documents

- Document2026-03-16-bown.xlsx (891.85 KB)

Author's note: Ashley Singh, Yuan Liu, and Greg Auclair provided outstanding data assistance, and Samantha Elbouez assisted with graphics.

With Soumaya Keynes, Bown is coauthor of the book How to Win a Trade War, available for pre-order and to be released on May 26, 2026.