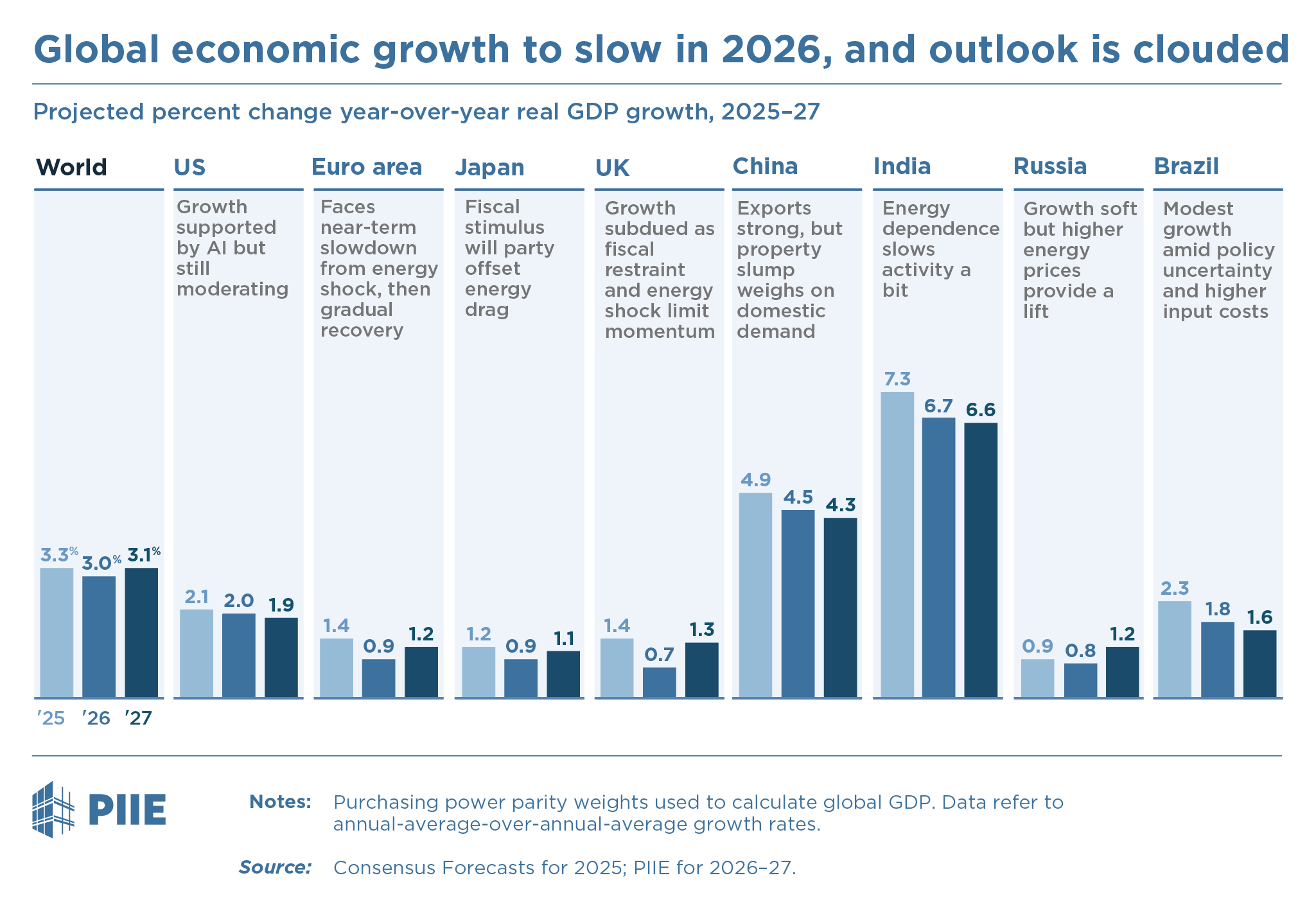

The global economy continues to expand, supported by the artificial intelligence (AI) boom, even as high energy prices, trade tensions, policy uncertainty, and structural challenges weigh on activity. Real global GDP growth is projected to slow from 3.3 percent in 2025 to 3.0 percent in 2026 before picking up to 3.1 percent in 2027 (see figure below), according to analysis presented at the Peterson Institute for International Economics Spring 2026 Global Economic Prospects event.

The disruptions associated with the Iran war—including to energy markets and supply chains—have lowered expected GDP growth, pushed up inflation, and made the outlook more uncertain. A two-week ceasefire announced earlier this week has eased tensions and brought energy prices down from their recent peaks, but they remain sharply elevated—still roughly 30 to 40 percent above pre-war levels. Markets remain highly sensitive to developments in the region, and uncertainty is high about whether the pause in fighting will endure.

War disruptions weigh on the outlook

The global economy entered the year on a reasonably solid footing, though with important differences across countries reflecting varying exposure to trade tensions, policy shifts, and structural headwinds. The outbreak of war in the Middle East introduced a new and significant shock. Roughly one quarter of the world’s oil is shipped through the Strait of Hormuz, which also carries substantial volumes of natural gas, fertilizer, helium, and other raw materials. Disruptions to these flows have reverberated through global energy markets and supply chains.

As a result, growth prospects have been marked down, and inflation is expected to be higher in many countries. Financial markets have reflected these developments: Energy prices surged, equity markets sold off, and interest rates moved higher before partially retracing those moves following the ceasefire.

In the baseline projection, energy prices recede later this year, broadly in line with futures markets, allowing growth to firm after a soft patch. But there is significant downside risk. In a scenario where tensions re-escalate and oil prices move to a high of $150 per barrel before receding, global growth could be roughly 0.4 percentage point lower.

US growth is expected to moderate amid competing forces

In the United States, economic growth has continued to be supported by the AI boom, which is boosting investment and, through wealth effects, consumption. The labor market is cooler than it was in the early 2020s but remains close to full employment, and household financial distress appears limited. Fiscal policy is also providing a modest boost to demand this year. At the same time, the sharp drop in immigration is constraining labor supply and weighing on potential output, offsetting some of the productivity gains from AI. As a result, growth is expected to moderate slightly toward a more sustainable pace as earlier tailwinds fade and policy uncertainty weighs on private decision-making. US real GDP growth is projected to slow from 2.1 percent last year to 2.0 percent in 2026 and 1.9 percent in 2027.

For the Federal Reserve, the current environment argues for patience. Inflation remains above the Fed’s 2 percent target, and the energy shock and related disruptions are likely to push inflation higher in coming quarters. At the same time, higher prices will erode real incomes, weighing on demand and softening labor market conditions. Inflation expectations remain broadly anchored but may be less firm than before the pandemic. Policymakers are therefore likely to remain highly data dependent. Although the most likely outcome is that the Fed will ease later this year after the energy shock passes through, the trajectory of monetary policy is particularly uncertain. All told, US inflation—as measured by the personal consumption expenditures price index (PCE)—is projected to rise to 3.2 percent in the fourth quarter of 2026 compared with the same period of 2025. Core inflation, which excludes volatile food and energy prices, is projected to reach 3.1 percent. Overall inflation is expected to cool in 2027 to 2.2 percent, with core inflation declining more gradually to 2.8 percent.

Different forces shape growth across economies

Growth across other advanced economies is weak in the near term, largely reflecting the hit from higher energy prices, but is expected to pick up next year as the shock fades and cyclical forces reassert themselves. In the euro area, higher energy costs are weighing heavily on activity this year, with growth expected to remain subdued before strengthening modestly in 2027. Japan faces similar headwinds, with fiscal support expected to provide some offset next year and help support a pickup in growth. The United Kingdom is also seeing weak near-term growth, as higher energy prices compound the effects of fiscal restraint and already soft domestic demand.

Among emerging-market economies, growth remains uneven. China continues to benefit from strong exports, but the property downturn is weighing on domestic demand. India remains one of the faster growing large emerging economies, though growth is likely to be dampened somewhat by its energy dependence. Brazil faces slow growth amid policy uncertainty, higher input costs, and ongoing structural challenges. Russia’s growth is likely to remain soft despite some support from higher energy prices.

The range of outcomes has widened, with important downside risks

The global economic expansion is set to continue, but the range of possible outcomes has widened. Underlying forces—especially the AI-driven investment cycle—continue to support growth, but the Iran war has introduced new risks.

Looking ahead, much will depend on how the geopolitical situation evolves. A renewed escalation in the Middle East could deliver a more pronounced stagflationary shock. At the same time, any loss of momentum in AI-related investment or a further rise in policy uncertainty could expose underlying weaknesses across economies.

Data Disclosure

This publication does not include a replication package.