Key Takeaways

- Questions about “bankability,” or investor and lender confidence, are now the main barrier to investment in critical minerals.

- The United States’ market-based financing tools contrast with China’s strategy of government-backed projects that yield lower profit margins.

- Triangulating between the desires of private capital markets (high returns), downstream users (low prices), and national security (low risk) will shape the politics around these supply chains.

“Bankability” has become a buzzword in US critical mineral discussions, appearing in many official and scholarly publications[1] and reflecting concerns that investments to produce these minerals require a sufficient risk-adjusted return to be “bankable.” The term’s entrance into the critical mineral lexicon reflects the growing recognition that building critical mineral supply chains that do not rely on China is as much a financing challenge as a geological or technical one.

The United States wants to break China’s near monopoly on the refining of many critical minerals, particularly rare earth (REEs) and heavy rare earth elements (HREEs) like samarium, terbium, and dysprosium that are so critical to energy infrastructure and national security. The nascent US approach to critical minerals under President Donald Trump has involved equity stakes and long-term agreements between domestic producers and buyers, as well as price supports, loan guarantees, and concessional financing, and efforts to coordinate supply chains with allied producers and processors. The ostensible goal is to create a “bankable”, i.e., investible price and risk environment that will encourage private capital. For that to happen, investors must believe these projects will offer net risk-adjusted returns comparable to those in other investable sectors.

By contrast, China’s dominant position is in large part a result of Chinese industrial policy that treats critical minerals like strategic infrastructure: tightly managed projects that are expected to earn modest returns, reinforcing its support of downstream, higher-value-added activities and the geopolitical leverage over countries around the world that depend on Chinese minerals.

The United States is thus trying to solve a strategic infrastructure problem with tools designed for return-maximizing capital markets, which may create a structural mismatch between market expectations and US geopolitical objectives. Capital seeks return on investment (ROI). The US government seeks predictable, low-cost supply as the best way to support higher-value-added downstream activities and ensure national security. We can thus expect a lot of political wrangling over the “appropriate” returns to these investments; they will define the extent of market interventions necessary to establish “bankability.”

In this context, “bankability” refers to lenders’ and investors’ confidence that anticipated returns are sufficient relative to risk. US government offtake agreements (between producers and buyers), strategic stockpiling,[2] and coordinated price floors all represent attempts to provide a clear, long-term, “bankable” signal to capital markets. These signals will be necessary to lure capital into the sector and provide a viable alternative to Chinese critical mineral dominance.

Of course, bankability is relative: a HREE processing facility may have strong fundamentals, but those fundamentals and anticipated rates of return will be assessed in comparison to other projects and sectors offering (sometimes much) higher ROI. To understand what “bankability” means in practice, it is useful to benchmark against other sectors.

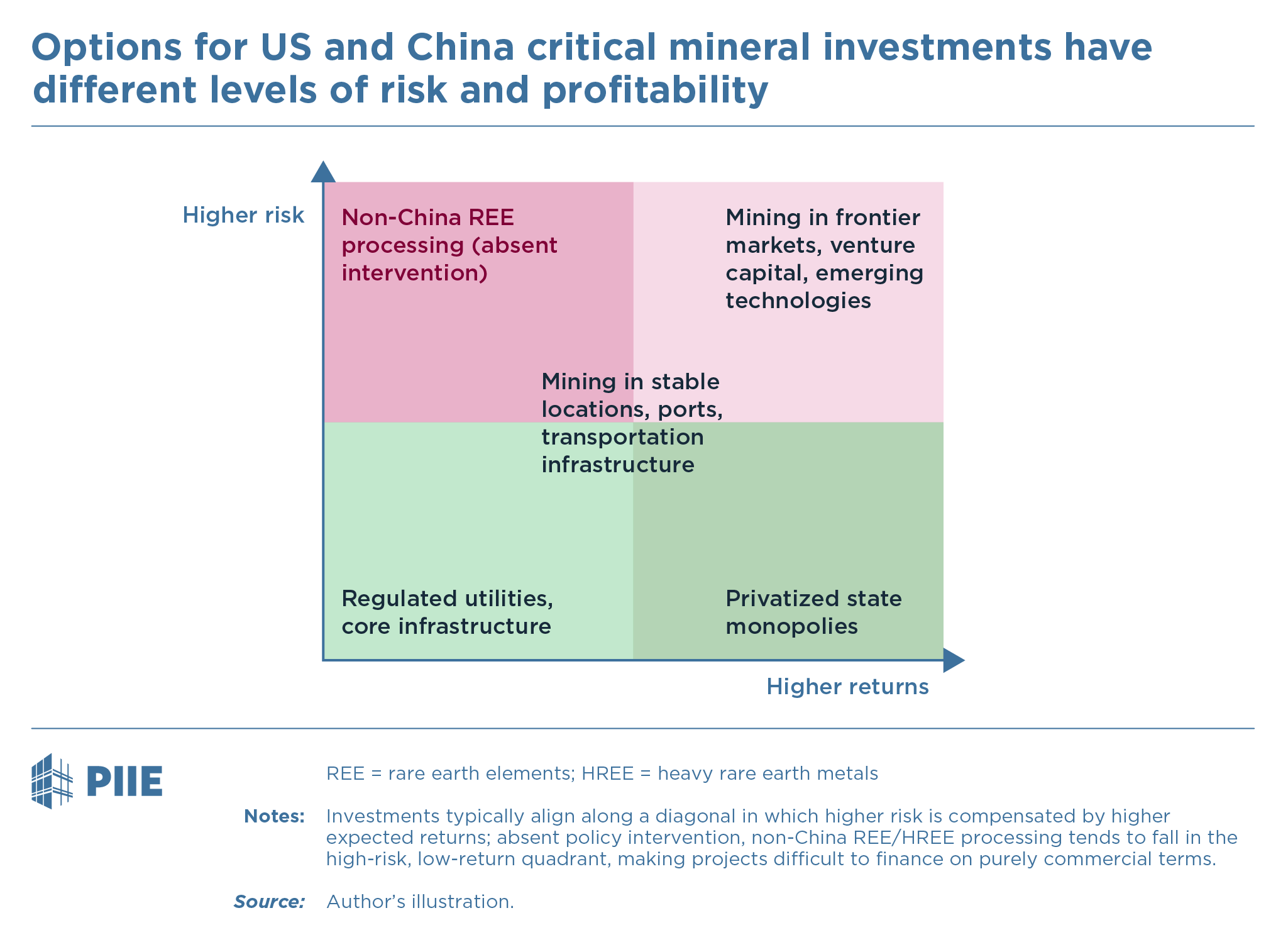

Typically, returns on investments are risk-proportional. Low-risk investments typically offer low (but predictable) returns; high-risk investments provide opportunities for much higher returns but also higher risk of loss of principal (figure 1). Absent market interventions, Western investments in REE/HREE mining and processing sit off that diagonal: Anticipated returns are small due to Chinese advantages in scale, but Chinese control of supply—and thus pricing—render them very exposed to market manipulation.

Chinese critical mineral processors, on the other hand, are treated more like elements of core infrastructure (low risk as strategic sectors, low average returns): necessary building blocks for an industrial economy whose social value is not captured by their market price. The Chinese model uses credit subsidies, subsidized policy banks like China’s Eximbank and the China Development Bank, and price management to spread risk (and cost) across the entire economy, rather than concentrating it at the project level. High-risk, low-reward investments are hard to justify to private capital, especially when equities and other classes of investments are performing well.

All of the projects in the diagram are “bankable” at different tolerances for risk and expectations about returns. The question facing US policymakers—and the coalition of the willing developing around non-China REE/HREE supply chains—is which quadrant of the risk-returns space should investments independent of China occupy?

If intended as self-insurance or blanket import substitution, such “bankable” supply chains would need to be rock-solid, i.e., very low risk. But the anticipated returns generally associated with such investments—like regulated public utilities where profit maximization is constrained in order to reap social benefit—are by design low to overcome the market power of monopolies, for example.

As is well known, investors would like—some would argue need—higher margins and profits. Higher returns for capital must be paid by someone, either in the form of taxpayers through tariff barriers and/or subsidies, higher input costs for downstream users, or some combination of both. Geopolitics are defining the need, but domestic distributive politics will determine how these higher costs are allocated. Triangulating between the needs of private capital markets (high returns), downstream users (low prices), and national security (low risk) will shape the politics around these supply chains.

Whatever mixture of risk and return US policy lands on, there is also the question of how stable that policy will be. I’ve argued before that potential partners at home and overseas will be reluctant to anchor their supply chain diversification strategies around US-led initiatives because of two perceived political risks: The first risk arises from policy instability that can lead to abrupt policy changes dependent on the politics of the moment. More fundamentally, there is a risk from concerns among investors and US allies about US coercive tactics in the creation and operation of a critical minerals network independent of China. Questions abound also about the need to build out energy and other complementary infrastructure, both in the United States and in comparatively infrastructure-poor but resource-rich less-developed and middle-income countries.

The United States has three basic ideal-type models it could implement: market-driven (high risk, high volatility, unlikely to meet need), infrastructure-like (low returns, high subsidies), or –worst from a social perspective—a model that locks in high returns in a protected market. The last was the model that emerged in Mexico during that country’s experience with privatization in the 1980s and 1990s, keeping costs high for consumers while making Mexican business tycoon Carlos Slim the world’s richest man for a time because his investments were protected from competition. Ultimately, the question is not whether these supply chains can be made “bankable,” but under which model? And who will bear the costs of sustaining it?

Notes

1. See the US Department of Energy’s Office of Energy Dominance Financing, US-Australia Critical Minerals Supply Framework, and a recent report by the Colorado School of Mines’ Payne Institute.

2. Stockpiles provide insurance against short-term disruptions but are not without their own political economies. Stocking policy, for instance could be a double-edged sword, helping stabilize prices, but releases from the stockpiles—triggered by scarcity (real or perceived)—could also cut into producer profits during times of high prices.

Data Disclosure

This publication does not include a replication package.