The unceremonious sidelining of Finance Minister Yanis Varoufakis of Greece from the negotiations between Athens and the euro area opens a new phase in the crisis. Whether a solution is in the offing remains to be seen. But as predicted, Varoufakis's efforts to rally support for his cause in international circles by openly criticizing Europe's and the International Monetary Fund's (IMF) handling of the Greek crisis failed. Greece's cash levels are running out, even after running arrears to local suppliers and the recent decision to raid the coffers of local governments (which may unlock up to €2 billion). Approval ratings of the government led by Prime Minister Alexis Tsipras are sinking, and polls continue to show overwhelming public support (over 70 percent) for a deal, even if that implies a compromise and further adjustment by Greece.

The popular mandate is to reach a deal. It is time for Tsipras's team to follow suit.

An anecdote from the IMF–World Bank meetings in April, when Varoufakis arrived alone at the IMF headquarters in Washington, DC to meet Managing Director Christine Lagarde, speaks volumes about why he had overstayed his welcome. Denied entry because he was not carrying the official badge, Varoufakis arrogantly demanded to be let in, only to retreat and use his cell phone to contact someone to help. At all meetings Varoufakis was told that yes, mistakes have been made with the Greek program, including by the Greek governments, but that rules are to be respected and an agreement requires negotiating in good faith rather than publicly hectoring his counterparts. His strategy of stalling to gain time for a better political solution by blocking any technical negotiation with the Troika (the IMF, the European Central Bank and the European Commission) has eroded their patience and goodwill.

Another turning point was reached at the acrimonious Eurogroup meeting in late April. Tsipras's modus operandi has been to wait until the last minute, to buy time to pivot from his anti-system campaign platform to a workable government strategy and then suddenly flip when the money runs out, as the path to the February 20 agreement showed. His reshuffling of the negotiating team so that technical level discussions can get under way followed that pattern. The technical team of officials is aligned with moderate Deputy Prime Minister Dragasakis and Giorgios Chouliarakis, an official well known and respected in Brussels. Deputy Foreign Minister Euclid Tsakalotos—who, unlike Varoufakis, is a member of Syriza and can therefore mediate between the negotiators and the rebels inside Syriza—is the new coordinator of the negotiators. The Central Bank of Greece is now being allowed to participate in the discussions. For the first time in months there is hope for progress.

More important, Tsipras said in a television interview in late April that he would be willing to hold a referendum in order to secure a deal for the new program in June, signaling that he is ready to broaden the political support for an agreement that will likely violate some of his electoral promises. A referendum would be faster to organize and provide much higher odds of success than snap elections and would allow Tsipras to contain the likely revolt in Syriza's far left wing. Of course, in order to hold a referendum he will first have to have a deal on the new program.

The path to an agreement is clear. Greece needs to show some tangible progress prior to the May 11 meeting of the Eurogroup—which consists of the euro area finance minister—to have a chance of a partial disbursement of the pending €7.2 billion and be able to make the May payments (although Greece could even meet the May payments without completing the review, using the money seized from the local governments). The rush to pass legislation in late April with measures to boost revenues is part of this strategy. Then a deeper discussion of a new program, which will have to include the thorny pension and labor market reforms opposed by Syriza's left wing, will have to be completed by mid-July. The contours of the new program suggest that it could be large, in the €30 billion to €50 billion range, if Greece fails to restore market confidence and needs a fully funded program. But it could also be quite a bit smaller, or even just a credit line, if there is enough confidence on the rollovers of the treasury bills coming due (recall this was the assumption last summer, before the election was called and the consensus was that Greece would have been able to exit the program with just a precautionary line of credit). With the IMF unlikely to participate in the new program, the debt sustainability discussion will be easier to handle as the debate over the need to restructure the official European debt could be postponed.

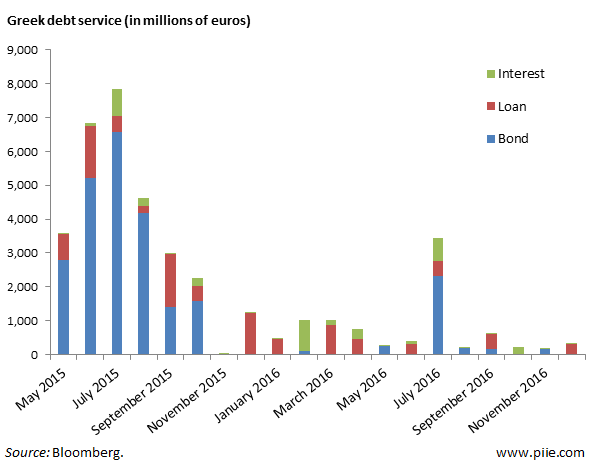

Markets have reacted favorably to the new Greek strategy. But the Tsipras government still has a long way to go to recover the political trust and market confidence lost since it was elected in January. Credit default swaps on Greek government bonds still show a 75 percent probability of default within 12 months. With large payments coming due in the next few months (see figure below), further delays in the negotiations or a bad outcome in an eventual referendum would put the Greek government in an untenable situation.

The political cost of running further arrears in the domestic economy would be high, and a default to the IMF would make Greece a pariah in international financial markets and trigger an "in-or-out" ultimatum from the euro area by its European counterparts. A gradual reduction or even a suspension of ECB financing of Greek banks, likely via a change in the haircuts of collateral submitted for Emergency Liquidity Assistance (ELA) financing, would ensue. A bank holiday or even capital controls would become unavoidable to contain the likely bank run. This need not lead to a euro exit, though, as many argue. For all the sound and fury that followed the installation of capital controls, Cyprus did not exit the euro as a result. Capital controls there were a transitory measure that worked well, and a similar scenario would be likely for Greece while a political consensus for a solution is reached.

On the other hand, if Greece reaches an agreement to unlock the pending disbursements, meet the large summer redemptions, and agree on a new multi-year program, debt service becomes very light thereafter (see figure), providing near term breathing room for growth. In addition, as discussed before, almost two-thirds of the Greek debt is in the form of loans from European countries and institutions with long maturities and low interest rates, and will not impede Greece's growth for many years. At the same time, if Greece wants to restore policy credibility and market access, it willneed to run a persistent primary surplus. With or without a program, Greece will need strong fiscal discipline.

The economic future of Greece is no longer in the hands of the Troika. It is in the hands of Prime Minister Tsipras and his ability to reform the economy and chart a stable political climate and a credible growth path. Enough of hiding behind the Troika. It is time for Tsipras to take ownership of the Greek economy.